In recent years Islamic Finance has firmly established itself as one of the most vibrant and yet often overlooked sectors within FinTech, as well as within the global financial services industry more broadly.

However, Islamic Finance is in fact a very broad term that encompasses a wide range of products, services and types of firms. What is true across this diverse segment of global financial services is that there is a lot of excitement for good reason. This is not at all surprising given the wave of innovation, growth and success of both the leading firms and the sector as a whole over recent years.

Whether you are new to the world of Islamic Finance or a professional, our Insider’s Guide to Islamic Finance provides expert insights and latest data analysis on the sector - highlighting just how successful Islamic finance has become at a global level.

WHAT IS ISLAMIC FINANCE?

Islamic finance refers to financial services activities, most notably banking, insurance and financing (credit), that must adhere to Sharia law (Islamic Law). The term can also be used to refer to Sharia-compliant investments as well as broader capital and equity markets.

The common practices of Islamic finance and banking arose alongside the establishment of Islam. However, institutional Islamic finance did not emerge until the twentieth century. Currently, the Islamic finance sector is growing at a rate of 15% to 25% per year, with Islamic financial institutions managing assets worth over 2.7 trillion USD globally.

SIZE AND GROWTH OF ISLAMIC FINANCE

The global market for Islamic Finance continued positive momentum in 2020, recording a growth rate of 10.7% year-on-year, driven primarily by strong performance within Islamic Banking as well as the Equity and Capital markets:

- Islamic Banking: 4.3% year on year growth with a growth in total assets of 248 billion USD, particularly in the largest Islamic markets such as Saudi Arabia and Iran.

- Capital Markets: 26.9% year on year growth

- Islamic Insurance (Takaful): 10% annual growth rate and over 51 billion USD in total assets in 2019 prior to the global financial slowdown caused by COVID-19.

Currently the top 3 countries where Islamic Finance is most well established account for 66% of the global market size across a wide range of metrics:

- Saudi Arabia

- Iran

- Malaysia

However, the Islamic Finance sector is growing rapidly in terms of overall scale, diversity and reach around the globe and into new periphery markets. In 2020 there were over 1,526 islamic finance institutions in operation around the world, with over 46 countries now supporting the growth and development of Islamic Finance within their legal and regulatory frameworks.

This is particularly true within FinTech, where firms and growth has gravitated towards London, the global hub of innovation in financial services, despite the relatively small Islamic community in the United Kingdom.

THE FOUR MAIN AREAS OF ISLAMIC FINANCE

Our guide breaks the data and the sector down into four key areas that are currently driving innovation and global success:

- Islamic Banking

- Islamic Capital Markets (ICM)

- Islamic Insurance (Takaful)

- Islamic Fintech

This page provides an overview of each, including the latest data trends and key highlights, which are expanded on further in each of the individual sections to provide detailed analysis and insight on each area of Islamic Financial Services.

In 2020 the total size of the Islamic Banking sector had a growth rate of 4.3% year on year and reached over 2.7 trillion USD in total assets. While Islamic banking is still largely regional in terms of market share and overall size, it now accounts for over 6% of the global banking market. Islamic Banking is also both the oldest and most important sub-sector within the global Islamic Financial Services industry, comprising 68.2% of the total market.

SIZE AND GROWTH

In the worldwide IFSI, the Islamic banking category maintained its dominance. Among the 36 jurisdictions included by the IFSI Stability Report 2021, the domestic market share of Islamic banking in relation to the total banking market segment has increased in at least 23 nations.

The performance of the Islamic banking category increased by 4.3 percent in 2020, compared to 12.4 percent in 2019. The Islamic banking segment now accounts for 68.2 percent of the global Islamic Financial Services Industry, down from 72.4 percent in 2019. This decrease is primarily due to the rising significance and strong performance within the Islamic Capital Markets during recent years, rather than indicating a drop in the performance within Islamic Banking.

Islamic Banking is still largely concentrated within geographic regions and markets, where it is the market leader within financial services. Taken together the 15 systemically important Islamic banking jurisdictions accounted for 92.4 percent of global Islamic banking assets, representing only a small increase from 91.4 percent in the previous year. These combined markets also now account for 82.7 percent of the total global assets linked to Sukūk that are currently outstanding, which indicates the availability of high-quality liquid assets (see SECTION 2 for more on Islamic Capital Markets).

DIVERSITY WITHIN ISLAMIC BANKING

As of 2020 there are now 526 Islamic Banking Institutions operating across 72 countries, with a systemically important market share in 15 of these jurisdictions. Within the Islamic Banking sector there is both innovation and diversity in terms of their operations and structures.

Breakdown of Islamic banking institutions:

Regionally, GCC (the Gulf Cooperation Council countries) retained its position as the largest domicile for Islamic finance assets in 2020. The region accounted for 48.9% of global Islamic finance market share, increasing from 45.9% in 2019. The Middle East and South Asia (MESA) region constituted the second-largest share, accounting for 24.9% of global IFSI assets, remaining consistent with the previous year.

The South-East Asia (SEA) region's share shrank slightly to 20.3% in 2020 from 23.8% in 2019, while that of the Africa region remained small, with a share of 1.7%. The “Others” region, comprising Turkey, the UK and countries from the Commonwealth of Independent States (CIS) region, accounted for 4.3% of total global IFSI assets.

SECTION 2 - ISLAMIC CAPITAL MARKETS (ICM)

- 428 commercial

- 57 investment

- 22 wholesale

- 19 specialized

Regionally, GCC (the Gulf Cooperation Council countries) retained its position as the largest domicile for Islamic finance assets in 2020. The region accounted for 48.9% of global Islamic finance market share, increasing from 45.9% in 2019. The Middle East and South Asia (MESA) region constituted the second-largest share, accounting for 24.9% of global IFSI assets, remaining consistent with the previous year.

The South-East Asia (SEA) region's share shrank slightly to 20.3% in 2020 from 23.8% in 2019, while that of the Africa region remained small, with a share of 1.7%. The “Others” region, comprising Turkey, the UK and countries from the Commonwealth of Independent States (CIS) region, accounted for 4.3% of total global IFSI assets.

SECTION 2 - ISLAMIC CAPITAL MARKETS (ICM)

Growth Rate: 26.9%

Share of IFSI: 30.9%

3,420 - Number of Sukuk issuances Outstanding (2019)

538 Billion USD - Total Value of Sukuk Outstanding (2019)

The sukuk market grew 30% in issuance value in 2019, increasing from 124.8 billion USD in 2018 to 162.1 billion USD. This is the 5th straight year where the sukuk sector has achieved double-digit growth in the sukuk industry, a leader within the overall strong performance in recent years across the Islamic Financial Services Industry.

Notably, although the volume of ṣukūk issuances dropped in 2020, ṣukūk issuances denominated in foreign currencies increased by 7% due to favourable liquidity and global market conditions created by a range of policy actions taken by central banks in Islamic majority markets in response to the COVID-19 pandemic and resulting economic slowdown.

The yield buckets for outstanding ṣukūk have shifted higher, with almost 80% yielding 3–10%

As with other sectors of Islamic Finance, Sukuk market share is both concentrated and significant within several key countries, where it is the debt instrument of choice for governments and has been relied upon to finance budget deficits during the COVID-19 pandemic.

Key Sukuk Markets:

- Malaysia

- Indonesia

- Saudi Arabia

- Iran is the Fastest Growing Market for Sukuk within Islamic Finance

Number of Funds: 140

Share of ISFI: 30.9% of total assets

Annual Growth Rate: 30% (2019)

In 2020 the ICM sector made up 30.9% of the total assets within the global Islamic Finance Industry, with growth and positive performance in key markets driven by sovereign and multilateral Sukuk issuances.

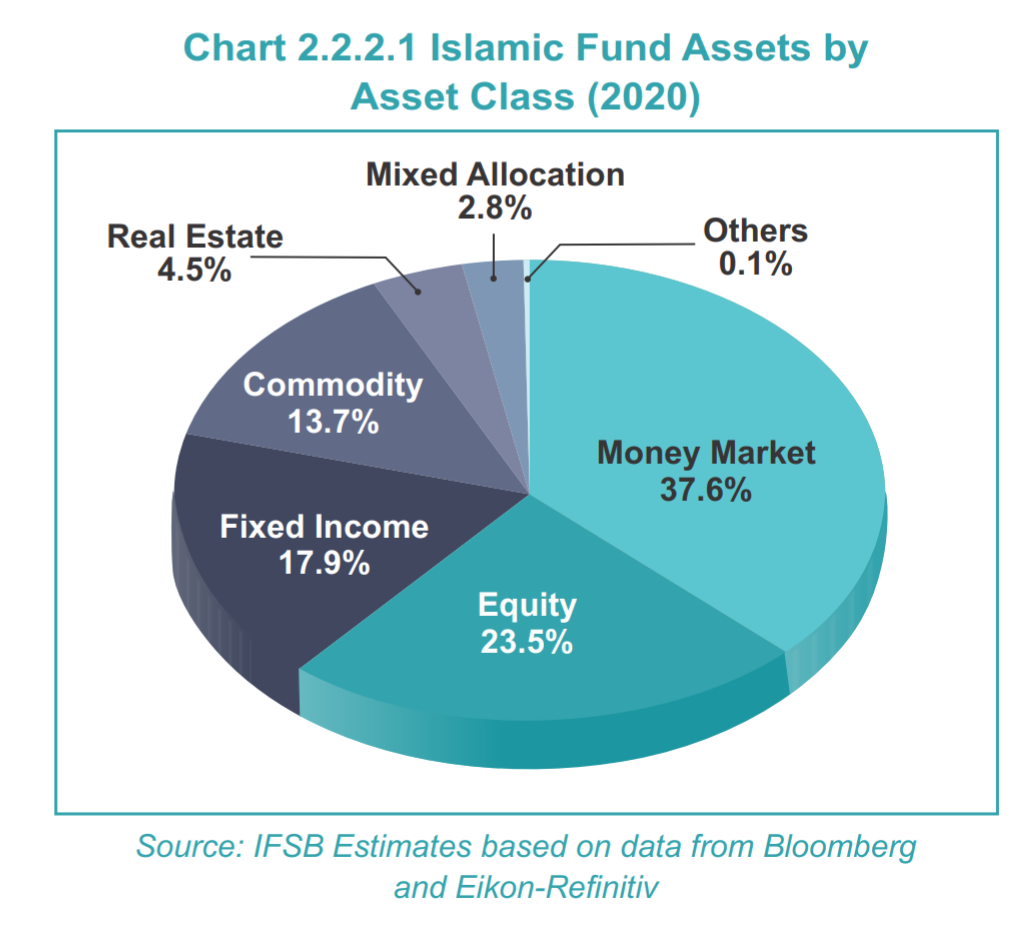

Islamic funds also recorded a noteworthy growth of 31.9% in terms of the total value of assets under management, while the Islamic equity markets also rebounded in the later part of 2020 after the initial shock and volatility in 1Q20 due to the outbreak of COVID-19 pandemic.

The total assets under management (AuM) of Islamic funds grew by 31.9% in 2020 despite the pandemic . While total AuM grew significantly, the total number of funds increased at a slower rate, which is a positive indication of growth in the average size of funds. The increase in scale of funds may be an indication of the flow of funds into emerging markets' fixed-income funds as a result of the search for yield and increased global liquidity.

Contrasting with the previous year, about 47% of funds now hold AuM of 1 billion USD or more each, while only 1% of funds hold AuM of less than 10 million USD (2019: only 2% held AuM of more than 1 billion USD each).

SECTION 3 - ISLAMIC INSURANCE (TAKAFUL)

Growth Rate: -14.8 %

Share of ISFI: 0.9% (2019)

The share of global takaful industry in the global IFSI declined marginally to 0.9% with a -14.8% growth y-to the exchange rate used for some member jurisdictions.

SECTION 4 - ISLAMIC FINTECH

Islamic FinTechs: 241 active in 2020

Transaction Volumes: 49 billion USD

Market share: 0.7% of total FinTech Transaction Volumes

SIZE AND GROWTH

Islamic Fintech is relatively small and recent but has shown strong initial signs of high growth and levels of innovation on a par, or superior to the wider FinTech sector even in the most competitive markets, such as London.

In 2020 the total transaction volume for Islamic Fintechs reached 49 billion USD, which is around 0.7% of the total global FinTech transaction volume.

While this represents an initial period of rapid growth, overall Islamic FinTech remains a relatively small part of the global Islamic Financial Services Industry. However, it is misleading to quantify the results as ‘poor performance’ in comparison to the strong growth within the mature sectors of Islamic Banking and Islamic Capital Markets. Instead, the demonstrated levels of innovation and competitiveness of Islamic FinTech also represents a huge opportunity for future growth.

At present the sector has yet to be fully developed across many regions and also many areas within the diverse FinTech landscape of innovation. Collectively, firms in the top 5 markets for Islamic FinTech account for 75% of the total market size, indicating a high concentration of market activity and room for future growth.

Top 5 Markets for Islamic FinTech:

- Saudi Arabia

- UAE

- Malaysia

- Turkey

- Kuwait

PERFORMANCE AND INVESTMENTS

The performance of Islamic Fintechs is particularly impressive, with projected transaction volumes set to reach over 128 billion USD in total by 2025. This represents a 21% CAGR, compared to the projected CAGR of 15% for the non-Islamic FinTech sector over the same period.

Investors have recognized this strong performance during recent years, with 56% of Islamic Fintechs expecting to complete an equity funding round in 2021. The expected average deal size for these investments was 5 million USD, providing a further indication that investors have high expectations for the performance of Islamic FinTech in the coming years.

- IFSB - the Islamic Financial Services Industry (IFSI) Stability Report 2021 [https://www.ifsb.org/download.php?id=6106&lang=English&pg=/index.php]

- DinarStandard & Ellipses - The Global Islamic Fintech Report 2021 [https://www.salaamgateway.com/specialcoverage/islamic-fintech-2021]

- ICD-REFINITIV - Islamic Finance Development Report 2020 [https://icd-ps.org/uploads/files/ICD-Refinitiv%20IFDI%20Report%2020201607502893_2100.pdf]